MARKET ASSUMPTIONS

The sharp increase in price was most likely caused by Terra shifting its business model from transactional-based to stablecoin supply-based. Formerly the yield was driven by e-commerce transactions from Chai, now it is driven by minting new stablecoins. Terra has set an ambitious goal: to become the stablecoin market leader and to offer the most widely adopted stablecoins. Terra’s stablecoins are already the most widely used algorithmic stablecoins, with a total supply (UST, KRT) of more than $2B, equal to approximately 2.6% of the total stablecoin supply. Terra is also in second place in the crypto-collateralized stable- coin market, just behind market leader DAI, which has a $3.7B stablecoin supply.

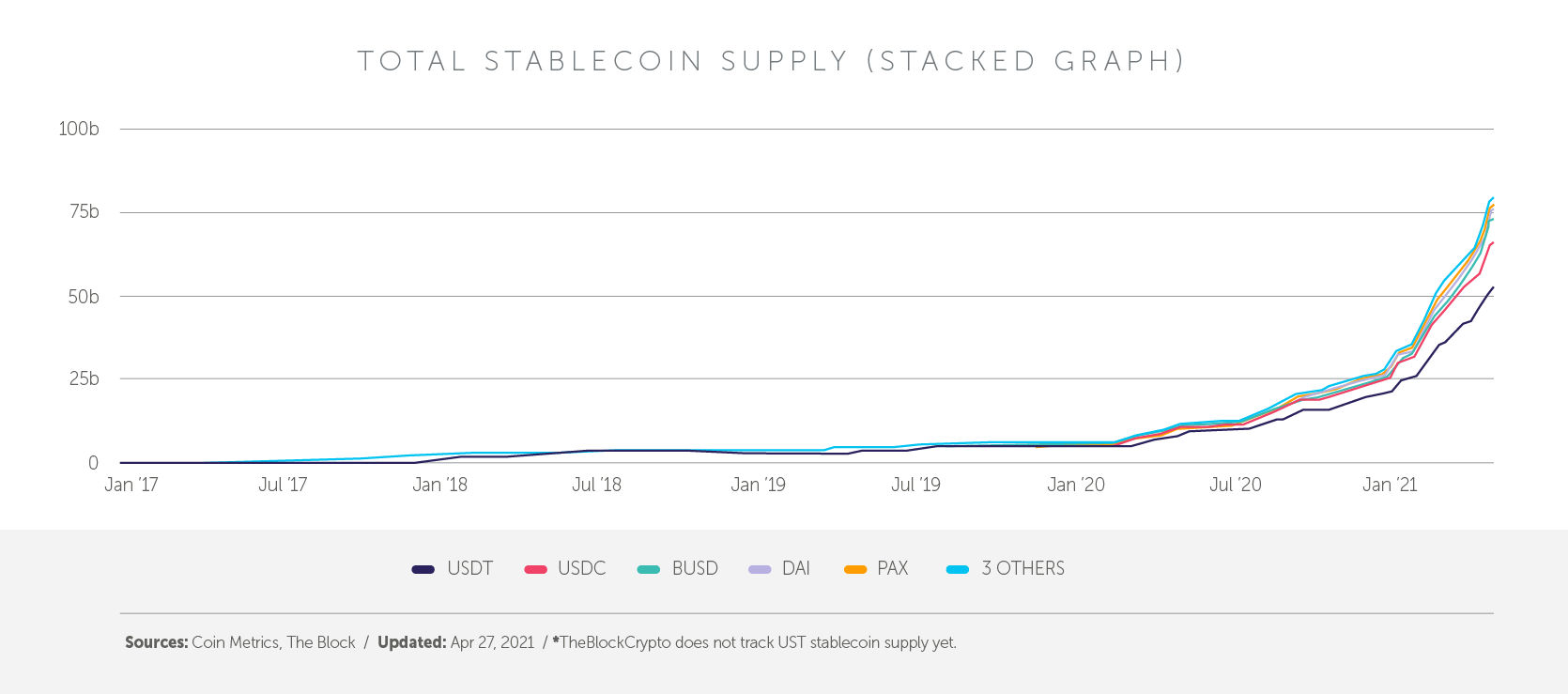

Based on TheBlockCrypto, the total stablecoin market in April 2021 was worth $75B and has achieved a CAGR growth rate of 91% since January 2019. For comparison, the total USD M1 money supply is $3.75T and has been growing by 5.4% since 2000. We project that the USD M1 money supply will grow by 4% p.a. and will reach $4.5T by the end of 2025. Over the same timeframe, we also assume that various stablecoins will reach 20% of this $4.5T future M1 money supply – i.e., $900B. We project that the digital asset stablecoin supply will grow at 70% CAGR between April 2021 and December 2025.

Source: theblockcrypto.com

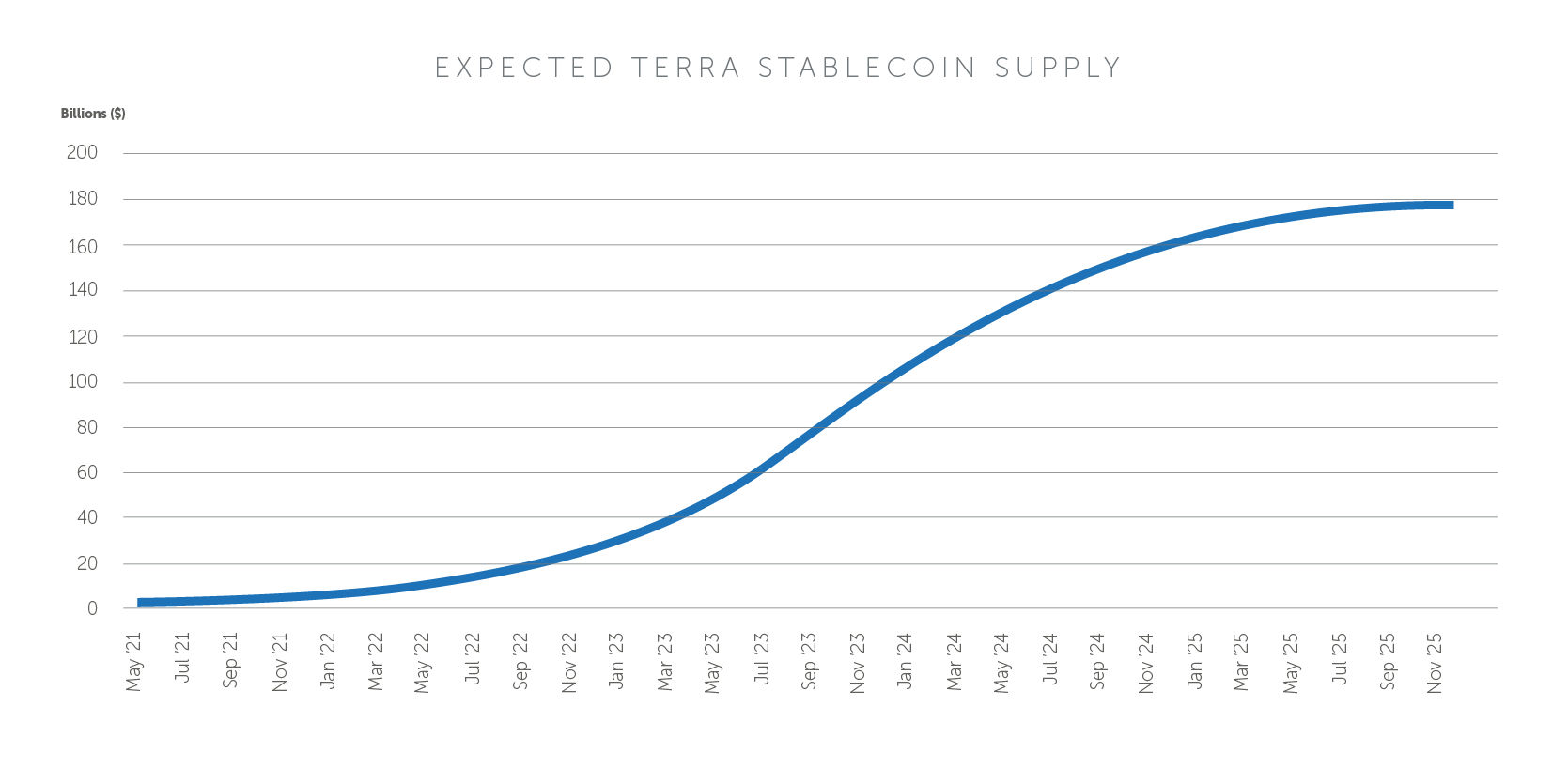

Due to Terra’s proven stability mechanism – the KRT stablecoin maintained its peg even in adverse market conditions such as the black Thursday on 12 March 2020 with only a -4% drawdown – and the business-focused mindset of Terraform Labs, we believe Terra will achieve a 20% stablecoin market share resulting in a $180B stablecoin supply by the end of 2025. We forecast Terra’s stablecoin supply growth rate to reach 128% p.a. over the same time frame. Hence, we believe that Terra will grow faster than the broader stablecoin market and that Terra will become the leading stablecoin provider at some point in the next 5 years. When we look at the stablecoin supply from the end of January to the end of April 2021, the supply has grown 96 % per month and Terra’s stablecoin market share has increased from 0.78% to 2.6% over the same period.

Given that the leading stablecoins are denominated in USD, we see the UST stablecoin to be the main stablecoin that will drive the future growth of the LUNA token price. It is worth saying that the CEO of Terraform Labs and founder of Terra, Do Kwon, expects UST to reach a $10B total supply by the end of 2021, which implies a UST supply increase of 5.6x by the end of 2021. In our predictions, we are slightly more conservative and expect the 10B UST supply milestone to be reached by June 2022.

ON THE VELOCITY OF STABLECOINS

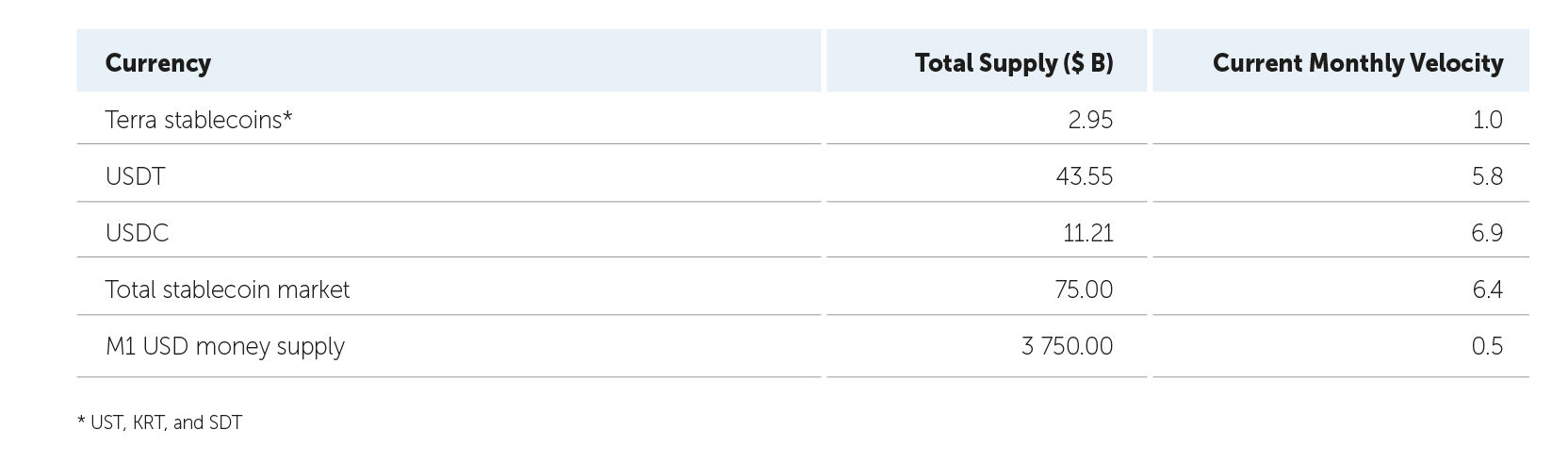

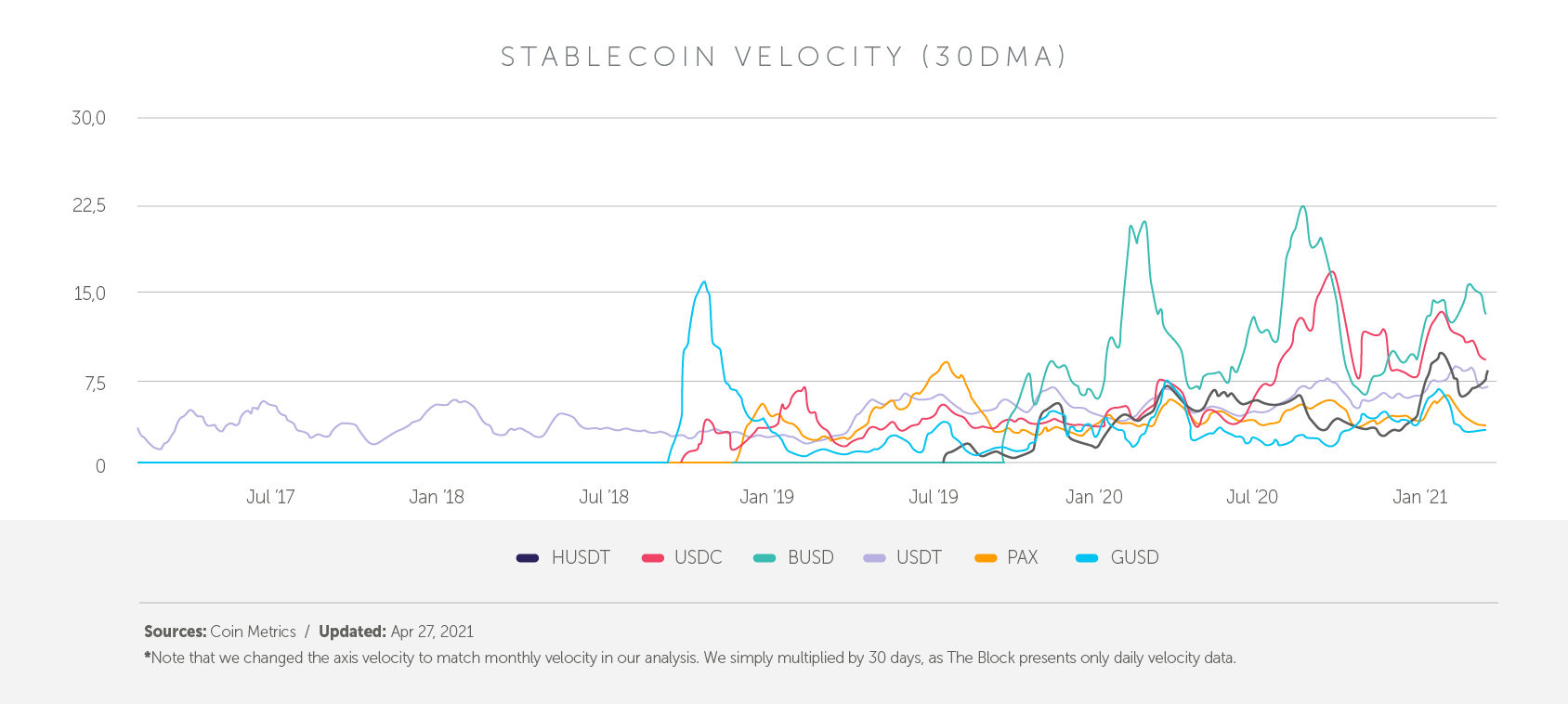

In comparison to USDT and USDC, Terra’s stablecoins have an 84% lower velocity, which means the Terra stablecoins change hands as much as 6 times less frequently then industry leaders. The velocity of UST resembles that of the USD M1 money supply more than USDC or USDT does. The table below summarizes the velocity of various stablecoins and USD.

The digital asset space contains less friction and thus supports faster and more flexible transactions than traditional finance systems. The current velocity of stablecoins (6.4 monthly) is high because it is driven by the primary DeFi use case – trading. In addition to trading, remittances also play a significant role in their high velocity. Although trading will still be a significant use case in the future, it will not be as dominant in comparison to savings as it is now. As more traditional users join the space and start using various DeFi services, savings proto- cols such as Anchor ($1.02B), AAVE ($12B in TVL; source: Coingecko), and Compound ($9.7B in TVL; source: Coingecko) will gain more traction. Locking funds into savings protocols will inherently decrease the velocity of stablecoins to levels closer to that of the M1 money supply.

Therefore, in our model, we project that the velocity of all stablecoins will decrease significantly (6% p.a. for UST and 32% p.a. for KRT) over the coming years and will resemble more the velocity of the USD M1 money supply by the end of 2025. In comparison to the M1 money supply, we project that Terra’s UST monthly velocity will decrease from 1 to 0.75 (+50% above current USD M1 velocity).

At Terra, we see the Anchor savings protocol to be the primary driver that will keep the velocity of Terra stablecoins low. It is in Terra’s interest to keep the velocity low, as more stablecoin supply can be minted and thus more LUNA burned. As such, we do not expect the Terra blockchain to dominate the trading use-case, but rather the savings use case.

Source: theblockcrypto.com

Revenue streams for stakers

MARKET ASSUMPTIONS

Unlike market leader Tether, Terra is not centralized and does not rely on a 1:1 holding of USD:USDT. Terra’s stablecoins are pegged using a stability mechanism (on-chain swap), that enables it to burn $1 worth of LUNA for $1 worth of UST at any point in time. The mechanism functions in reverse as well. To keep the stablecoins at their peg, the burn/mint mechanism relies on arbitrageurs to exploit profitable opportunities if Terra stablecoins deviate from their peg.

All burn and mint transactions are subject to fees. Currently the fees incurred during every on-chain swap total 0.85 % (Tobin tax of 0.35% plus a minimum swap spread of 0.5% “1” ), but these fees are subject to change by governance voting. The fees collected are then distributed to validators over a 3-year period, thus delivering a predictable cash flow stream to LUNA stakers even in the case of a down market. We expect the protocol to collect approximately $1.5B worth of fees until the end of 2025 and $1.23B of the total to be distributed to stakers by end of 2025. This projection assumes that every new UST will have to flow through the mechanism only once – when it is minted.

“1” – Every stablecoin can have distinct minimum swap spread. TIP 68 recently passed, increasing the KRT swap spread to 1% https://station.terra.money/proposal/68

TRANSACTION TAX

Every transaction on Terra is subject to 0.403% in fees capped at $1.4 (1 SDT). We expect similar composition of transaction sizes and, therefore, we do not project any change in the average fee charged per transaction. Based on the monthly velocity outlined earlier, we project a $139B monthly volume and $10.3M in gross monthly protocol revenue from transactions on the Terra blockchain by the end of 2025. This revenue will accrue to LUNA stakers over period of 3 years, contributing to stable cash flow. Between April 2021 and December 2025, we expect transaction fees to generate a total of $320M.

LUNA BURN/MINT

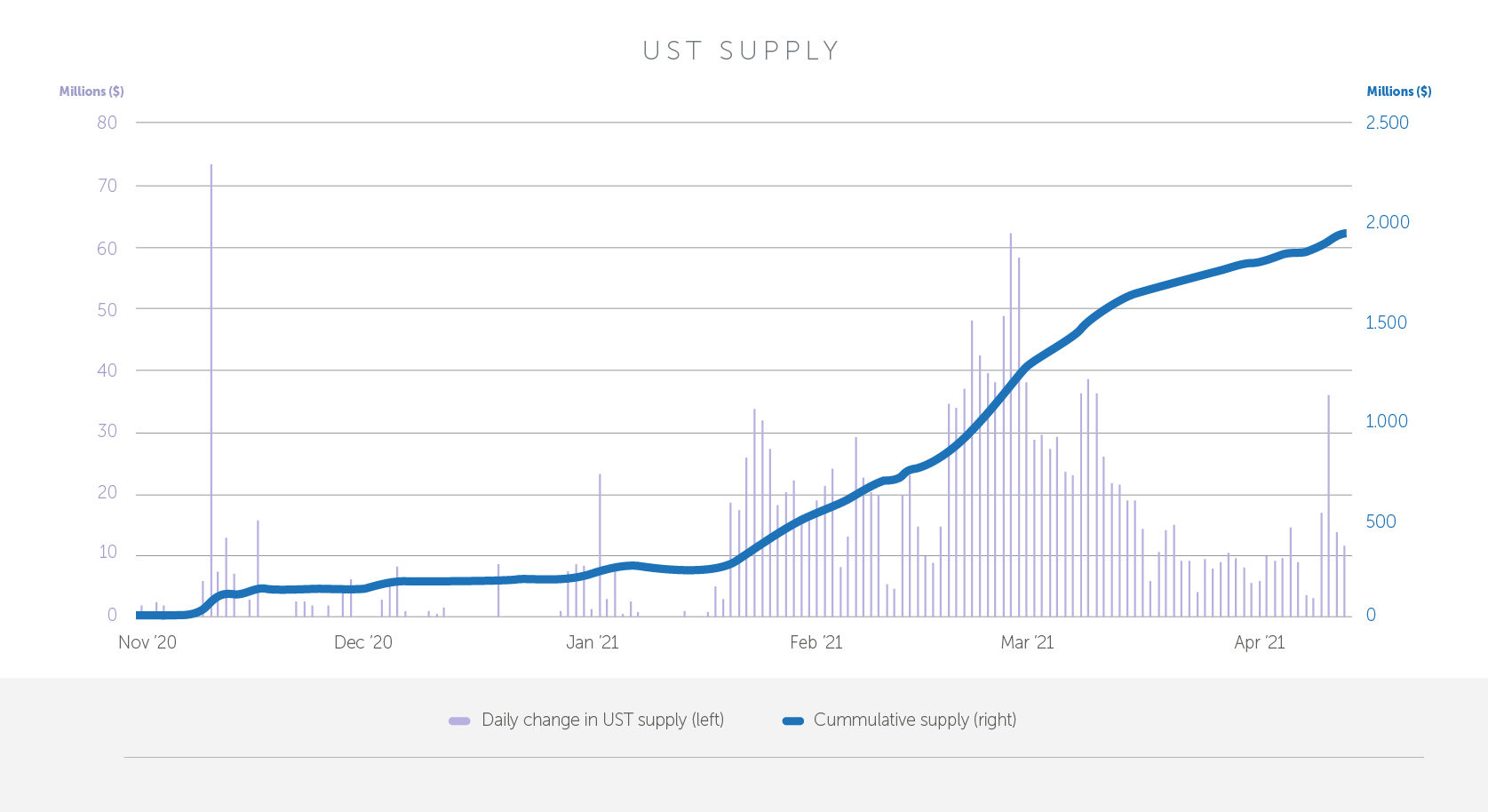

The biggest value driver of the LUNA price will be the yield from burning and minting LUNA tokens as the total stablecoin supply increases. As outlined previously, we project $177B in new Terra stablecoins by the end of 2025. Therefore, $177B worth of LUNA tokens will have to be bought and burnt to mint $177B worth of stablecoins. In other words, the LUNA supply will decrease and there will be enormous buying pressure as the demand for Terra’s stablecoins increases. This will inherently drive the price higher. The yield accrues to anyone holding LUNA tokens and not just to LUNA stakers.

In our model, we account for this supply decrease as cash flow to stakers, because the net economic effect is similar. This projected increase of the total stablecoin supply is the main value driver behind the LUNA token price. Past daily minting amounts (left axis) together with the cumulative UST supply (right axis) are shown on the chart below.

Source: Terra Analytics

AIRDROPS

Mirror (MIR)

In the short term the value of LUNA is also driven by airdrops that every LUNA staker receives. Based on our future MIR price projections, we believe there is still $123M (discounted value) worth of MIR tokens to be distributed until the end of 2021. In December 2021, the airdrop supply will run out and the distribution of MIR tokens will stop. We see the NPV of Mirror to be $10.4/MIR token, applying a 60% discount rate. If you are interested in the details of the valuation model, feel free to contact us (Twitter @RBF_cap, or @DavidRakusan).

ANCHOR (ANC)

Similarly, LUNA stakers are entitled to ANC airdrop rewards. Unlike MIR airdrops, ANC airdrops are distributed over the course of two years and will last until March 2023. Based on our projections of the ANC token price, we discounted the value of future ANC airdrops to a current value of $964M. We see the NPV of Anchor as being $3.04/ANC, applying a 60% discount rate. If you are interested in the details of the valuation model, feel free to contact us (Twitter @RBF_cap, or @DavidRakusan).

Given the established token distribution model, it is likely that more projects, like Pylon, Nebula, or Spar, will use airdrops as a means of bootstrapping attention and gaining initial traction, which will bring even more upside to LUNA stakers. Potential airdrops are mentioned on this list.

TERRASWAP (POTENTIAL ADDITIONAL REVENUE STREAM)

On top of the burn mint mechanism, also called on-chain swap, Terra enables anyone to swap tokens on Terra through Terraswap. Terras- wap is an AMM-type decentralized exchange like Uniswap, with some modifications. Terraswap achieves approximately a $2B transaction volume and incurs 0.3% in fees, which go entirely to liquidity providers. Some fee from Terraswap, say 0.05%, may possibly flow to LUNA stakers in the future. Assuming a similar ratio between Terraswap and the volume of on-chain transactions, we project $40B monthly volume by 2025. Such volume would generate almost $20M monthly to LUNA stakers by the end of 2025 and over $553M between April 2021 and December 2025. However, this revenue stream is only hypothetical and is not taken into account in our final valuation and price target.

Traction

There is decent growth in the number of projects building on Terra. Key protocols living on Terra like Anchor and Mirror are also being integrated into various more products. These projects include, for example, Kash, Loop Finance, Alice, Chai, Nash and others. Terraform Labs also hinted at various other protocols in the pipeline. Unfortunately, little specific information is in the public domain for the time being. Protocols in the pipeline include Ozone, a stable coin insurance protocol described by Do in this AMA, and this post, and Pylon (Twitter), an application being built on top of Anchor, through which a user will be able to pay with accrued interest or future cash flow.

Ten of the apps being built on Terra are mentioned in the Medium article by Ryan West and 32 are mentioned by ProfesoreFarmer. In the community AMA, Do recently showed confidence in the growing ecosystem. Although traction seems to be picking up, Terra’s ecosystem still seems lag slightly behind, for example, Solana. The probable reason for this is that Terraform Labs focused more on building their own key protocols (Mirror, Anchor) instead of attracting projects to build on Terra.

Risks

REGULATORY RISK

From a regulatory perspective, if the Terra stable coin supply becomes too big, Terra could be opposed by governments around the world. Governments could perceive the new monetary system created by Terra as a systemic risk they cannot manage, which would consequently threaten the power of central banks and governments to influence monetary policies. For example, the Thai central bank has recently published a warning against the use of Terra’s Thai bath stablecoin THT (source). On a similar note, Facebook had to redesign its Libra project (now called Diem) because governments feared the significant negative impact the project could have had. Unlike Libra, Terra is a more decentralized system and this might mitigate some of the regulatory risks, as it is harder to identify a responsible party within a decentralized system.

However, the proposed 2021 update of the Financial Action Task Force (FATF) recommendations defines, for example, the responsible parties in relation to decentralized applications, management of reserves backing a stable coin, and control of price stabilization mechanisms for a stablecoin, and hence these new recommendations might have some impact on Terra when (and if) they are adopted by governments around the world. Although the FATF recommendations are not binding, failure to adopt these recommendations could result in a country being subject to economic sanctions.

FATF is an intergovernmental organization founded in 1989 on the initiative of the G7 to develop policies to combat money laundering, and in 2001 its mandate was expanded to include terrorism financing. FATF comprises all major players, e.g., the USA, EU, UK, Russia, Switzer- land, South Korea, Singapore, Turkey, Australia, China, and many more.

SYSTEM STABILITY RISK

Terra’s stability mechanism works well when Terra’s economy is expanding – i.e., growing the stablecoin supply by burning LUNA. However, it remains to be seen how the whole system behaves during contractionary – burning Terra stablecoins by minting LUNA. Terraform Labs conducted extensive modelling according to which the stability mechanism will work well, but real-life data about the behavior of LUNA investors during contraction are lacking.

As Terra grows and the pace of minting stablecoins slows down, the inherent yield from burning LUNA will slow down as well, or even reverse when the system shifts to contraction.

To justify the higher price of LUNA, the stable predictable CF per token, generated from transaction fees, swap fees, and potentially other sources of revenues, will have to offset the slowdown from minting stablecoins. It is worth mentioning that we do not expect any contraction of the Terra economy (i.e., a decreasing Terra stablecoin supply) by 2025.

BUSINESS RISK

Regarding business risk, Terra’s stablecoins are not as popular now as other centralized solutions like USDT and USDC. Users might not see the value in using UST instead of USDT for applications outside of the Terra ecosystem, especially when the subsidy for Anchor and Mirror ends. We believe that users will, over time, see the benefits of having an algorithmically stabilized currency over solutions that require custodians.

For example, minting USDC requires holding USD. Companies like Circle (USDC issuer) can generate a small yield on USD deposits by investing in short-term deposits. However, this yield is very low (0.06% p.a. source) in comparison to what LUNA stakers receive (15% terra.smartstake.io). However, LUNA stakers assume high volatility in the case of the LUNA token, whereas a centralized stablecoin provider does not assume any volatility.

An analogy for this situation can be, for example, the struggle between centralized and decentralized exchanges. CEXes are now preferred by users but DEXes are catching up, are gaining significant traction, and enable users to participate in DEX success. In addition, investors can very easily act as liquidity providers and get rewarded for doing so. Volume on DEXes grew 95x YoY since April 2020. Unlike CEXes, DEXes are interoperable and composable, resulting in a completely new level of usability.

On a similar note, we expect fierce competition between centralized and decentralized stablecoin providers. On top of competition from centralized stablecoin providers, central bank digital currencies (CBDC) will also compete for market share in the future. According to a Morgan Stanley research report, 86% of central banks are exploring the issuance of CBDCs.

According to FED Chairman Powell, the digital dollar is a “high priority project”. Although, we don’t expect to see the digital dollar launch any time soon, CBDCs can pose risk to Terra in the long term as central banks will fight for control over fiscal policy. Also, if CBDCs gain more legitimacy and experience greater adoption, Terra stablecoins can become obsolete over time. For now, it remains to be seen how interoperable with DeFi the CBDCs will be.

Conclusion

Based on the above assumptions, forecasted revenues, and risks, we project the present value of the LUNA token at $74.3 (4.24x the current price of $17.5). We used a 60% discount rate, which we believe is appropriate for startup projects in the digital asset industry. Over a five-year investment horizon, we also believe the LUNA token can be worth more than $170 as the LUNA token supply decreases and cash flow will be distributed among fewer staked LUNA tokens. Investors in the LUNA token might see another 10x multiple on invested capital from current valuation levels. Based on our growth projections, we revised our target price of LUNA token to $170 with expectations that the price will achieve these levels at some point by the end of 2025. If you are interested in the details of the valuation model, feel free to contact us. (Twitter: @RBF_cap, or @DavidRakusan).

DISCLAIMER:

This article is for informational purposes only; it is not investment advice and we disclaim any and all liability for the information provided. It involves a number of assumptions, risks, uncertainties, and other statements; actual results may differ materially from such statements. No representation or warranty (expressed or implied) is made as to the fairness, accuracy, completeness, or correctness of the information provided or opinions contained in this article and nothing contained in this article should be relied upon as a promise, representation, or indication of the future performance of any asset. No information contained in this article constitutes an offer or invitation to purchase or subscribe to any interest in any asset and no part of it shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. Any logos and trademarks are displayed in this article for informational/educational purposes only and do not constitute any endorsement of any offering or any investment product.

David Rakusan is Investment Manager at Rockaway Blockchain Fund, responsible for portfolio management. He previously worked as an Investment Analyst at RSJ Investments, a financial group with €500M in assets under management, where he was responsible for analyzing both direct investment opportunities and indirect fund of funds investments in the VC sector. David holds a a Master’s Degree in Finance and Financial Management Services from the University of Birmingham and a CFA charter.